Explore www.niva bupa.com for Health Insurance Plans – Health insurance has become a need rather than a luxury. Increasing health and medicine costs, sudden hospitalization, and the necessity to have good healthcare make the insurance cover important to individuals and families. Among the platforms that have been drawn into the sector of health insurance in India is Niva Bupa Health Insurance whose official site Niva Bupa offers a range of plans according to various needs.

The website www.nivabupa.com enables users to research policies, compare cover plans, estimate premiums and buy plans online. It provides both health insurance to individuals, families and even the senior citizens and even to international travelers.

This is a comprehensive guide on what Niva Bupa health insurance plans are, their advantages, comparisons, main features and how to select the right plan.

What is Niva Bupa Health Insurance?

Niva Bupa Health Insurance is a health insurance company in India that deals specifically with medical coverage program which aims at insuring individuals and families against the increase in healthcare expenses.

The company offers several policies which include:

- Hospitalization expenses

- Pre and post hospitalization costs

- Daycare procedures

- Critical illness treatment

- Maternity and newborn care

- Preventive health checkups

The company serves millions of customers across India and offers access to a large network of hospitals for cashless treatment.

Health insurance policies from Niva Bupa aim to reduce the financial burden of medical emergencies while ensuring quick access to quality healthcare.

Why Explore www.nivabupa.com?

The official website of Niva Bupa is designed to help customers easily compare and purchase policies online.

Key Benefits of the Website

| Feature | Description |

| Plan Comparison | Compare multiple health insurance plans in one place |

| Instant Premium Calculator | Estimate annual premium cost |

| Online Purchase | Buy policies digitally without paperwork |

| Network Hospital Finder | Search for hospitals that offer cashless treatment |

| Policy Management | Track claims, documents, and policy details |

The website also provides helpful tools such as claim tracking, hospital search, and health check-up booking through its digital ecosystem.

Niva Bupa Health Insurance Plans

It offers multiple plans designed for different life stages and budgets.

| Plan Name | Sum Insured (Starts From) | Key Features | Approx. Starting Premium |

| ReAssure 3.0 | Unlimited | Unlimited sum insured with no limits, coverage for pre‑existing conditions from Day 1, global treatment with Go Borderless, executive health assessment & priority claims. | ₹7,430/year |

| Aspire | ₹5,00,000 | Lock entry age for premium, carry forward unused sum insured, maternity benefits including IVF & adoption, unlimited reuse of base coverage. | ₹8,632/year |

| Rise (Entry‑Level Family Plan) | ₹5,00,000 | Flexible payment, 50 % premium return that accumulates with bonus, ₹5,000 benefit if treated in govt. hospital with no claim, unlimited digital GP consultations. | ₹4,804/year |

| Health Premia | ₹5,00,000 (up to ₹3 Cr option) | Comprehensive cover including modern treatments, in‑built travel insurance, maternity & newborn cover. | ₹11,571/year |

| Health Companion (Smart Plan) | ₹5,00,000 | No room rent capping, modern treatments covered, hospitalisations ≥2 hrs covered, one‑time refill for same illness. | ₹11,775/year |

| Large Cover Smart Plan | ₹1,00,000 – ₹3,00,000 | Includes health check‑up, no room rent cap & no‑claim bonus options. | ₹8,207 – ₹8,207/year |

| Super Top‑Up Health Recharge | Up to ₹95 L (after deductible) | High sum insured for catastrophic expenses with deductible; covers pre & post hospitalisation, teleconsultations & diagnostic discounts. | ₹884/year |

| Cost‑Effective Mediclaim (1 Cr Sum Insured) | ₹1,00,00,000 | Comprehensive coverage, carry forward unused base & MIRACLE sum insured up to 10×, age‑based premium structure. | ₹13,305/year |

| Personal Accident Cover | Up to ₹5 Cr | Covers death & disability, plus child education support; can be added as optional cover. | ₹680/year |

| Criti Care (Critical Illness) | Up to ₹2 Cr | Covers 20 critical illnesses with lump‑sum or staggered payout options. | ₹1,002/year |

| Corona Kavach | ₹50,000 | COVID‑19 specific plan covering hospitalisation, home care, and pre & post hospitalisation expenses. | ₹208/year |

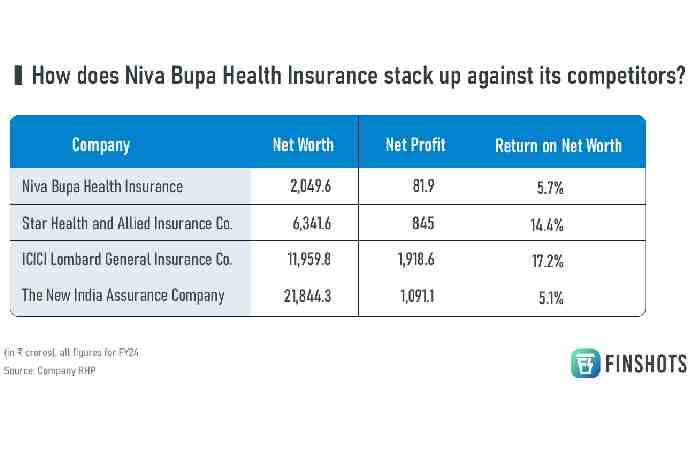

Niva Bupa Health Insurance vs Other Health Insurance

Here’s a comparison table showing key aspects of Niva Bupa Health Insurance versus other major health insurance companies in India — focusing on features, claims, networks, and benefits so you can see how they stack up:

| Aspect | Niva Bupa Health Insurance | Other Health Insurers (e.g., HDFC ERGO, Reliance, Aditya Birla, Star Health) |

| Claim Settlement Record | Generally strong claims payout; digital claim tracking and quick assistance. Some reports show competitive ratios in market. | Others like HDFC ERGO, Aditya Birla, Star Health report higher or comparable settlement ratios and longer market history. |

| Network Hospitals | ~10,000+ network hospitals for cashless treatment across India. | Many competitors offer larger networks (e.g., Star Health ~14,000+, Aditya Birla ~18,000+), giving slightly wider cashless access. (https://www.insurancedekho.com) |

| Coverage Options | Flexible plans (e.g., ReAssure, Aspire, Rise) with unlimited sum insured options, global treatment add‑ons, maternity and wellness features. | Other insurers also offer broad coverage plans, with some providing strong OPD benefits, wellness or additional riders, and critical illness covers. |

| Hospitalisation Rules | Covers hospitalisation with minimum 2 hrs stay (some unique product features). | Many insurers require 24 hrs minimum stay for inpatient claims, though digital tools can speed approvals. |

| Digital / Customer Experience | Strong online platform for policy purchase, renewal, cashless claims, and quick approvals. | Most competitors also offer mobile apps and online claims, some with established telemedicine and wellness rewards. |

| Special Features | Wellness incentives (premium discounts for healthy habits), cumulative bonuses, customizable plans. | Others offer annual health checkups, OPD covers, family floater options, and free checkups depending on plan. |

| Premiums & Value | Can be competitive or slightly lower in some products, especially entry‑level plans. | Premiums vary widely; some larger insurers have higher costs but stronger historical service and bigger networks. |

| Market Position | One of the top standalone health insurers with rapid growth and strong retail focus. | Larger general insurers (e.g., HDFC ERGO, Star Health) typically have bigger overall market share and diverse product portfolios. |

Key Features of Niva Bupa Health Insurance

When exploring plans on the website, several common benefits stand out.

1. Cashless Treatment

One of the biggest advantages of Niva Bupa policies is cashless treatment at network hospitals, meaning the insurer settles bills directly with hospitals.

This reduces the need for upfront payments during emergencies.

2. Pre and Post Hospitalisation Coverage

Most Niva Bupa plans cover expenses before and after hospital admission.

| Expense Type | Coverage Duration |

| Pre-hospitalization | Up to 60 days |

| Post-hospitalization | Up to 180 days |

These benefits ensure that diagnostic tests, doctor consultations, and medicines are also covered.

3. Modern Treatment Coverage

Modern medical treatments are often expensive. Many Niva Bupa plans include coverage for advanced procedures such as:

- Robotic surgery

- Stem cell therapy

- Organ transplant treatment

- Advanced cancer therapies

This ensures patients can access modern healthcare technologies.

4. No Claim Bonus

Policyholders who do not make claims during a policy year may receive a No Claim Bonus (NCB).

| Claim History | Bonus Benefit |

| No claim for 1 year | Increased sum insured |

| Multiple claim-free years | Higher coverage without extra cost |

This benefit rewards customers for maintaining good health.

Digital Healthcare Services from Niva Bupa

Niva Bupa also focuses on digital healthcare services to make insurance management easier.

Key Digital Features

| Service | Description |

| Online doctor consultation | Speak to doctors digitally |

| Health check-up booking | Preventive health screening |

| Medicine delivery | Order medicines online |

| Wellness tracking | Earn rewards for healthy habits |

Many plans also offer unlimited digital consultations with general physicians through their mobile application.

Benefits of Buying Health Insurance Online

Purchasing health insurance through the official website offers multiple advantages.

1. Faster Purchase Process

Buying online eliminates paperwork and allows users to compare plans instantly.

2. Transparent Pricing

The website clearly displays:

- Premium costs

- Coverage limits

- Add-ons

- Policy conditions

3. Discounts and Online Offers

Customers may receive online purchase discounts and flexible payment options when buying through the website.

4. Easy Policy Management

Policyholders can manage their policies through:

- Mobile apps

- Online dashboards

- Digital claim submission

How to Choose the Right Niva Bupa Health Insurance Plan?

Selecting the right health insurance plan requires careful evaluation.

Factors to Consider

| Factor | Why It Matters |

| Age | Premium increases with age |

| Family size | Family floater plans may be cheaper |

| Medical history | Pre-existing conditions affect coverage |

| Sum insured | Higher coverage protects against medical inflation |

| Network hospitals | Check hospitals near your location |

A plan with higher coverage ensures better protection against rising healthcare costs.

Step-by-Step Guide to Buying a Plan on www.nivabupa.com

Buying health insurance online is simple.

Steps

- Visit the official website.

- Enter your basic details such as age and city.

- Choose the type of insurance plan.

- Compare policies and coverage options.

- Calculate the premium.

- Fill in personal and medical details.

- Make the payment online.

- Receive policy documents via email.

The entire process can be completed in a few minutes through the digital platform.

Pros and Cons of Niva Bupa Health Insurance

Every insurance provider has strengths and limitations.

Advantages

| Advantage | Explanation |

| Large hospital network | Access to thousands of hospitals |

| Multiple plan options | Plans for families, seniors, and individuals |

| Quick claim processing | Fast approvals in many cases |

| Digital healthcare services | Online consultations and wellness features |

Niva Bupa claims to have millions of customers and thousands of claims processed over time.

Possible Limitations

| Limitation | Explanation |

| Premium increases | Prices may rise during renewals |

| Network hospital restrictions | Cashless treatment depends on network hospitals |

| Policy complexity | Some plans have multiple add-ons |

For example, reports in the news indicated that cashless services were temporarily suspended in certain hospitals, which affected policyholders relying on that facility.

This highlights the importance of reviewing policy terms and hospital networks carefully.

Who Should Consider Niva Bupa Health Insurance?

Niva Bupa plans may be suitable for:

Young Professionals

Affordable entry-level plans provide basic medical coverage.

Families

Family floater policies allow multiple members to share one policy.

Senior Citizens

Specialized policies provide coverage for age-related health conditions.

Frequent Travelers

Some plans include international treatment and travel benefits.

Tips to Get Maximum Benefits from Health Insurance

Having health insurance is only the first step. Using it effectively is equally important.

Smart Tips

| Tip | Benefit |

| Buy early | Lower premiums |

| Choose higher sum insured | Better protection |

| Use network hospitals | Cashless treatment |

| Renew policy regularly | Avoid coverage lapse |

| Maintain healthy lifestyle | Earn wellness rewards |

Planning ahead ensures you receive maximum value from your insurance policy.

The Future of Digital Health Insurance

Health insurance in India is rapidly evolving with technology.

Future trends may include:

- AI-based claim processing

- Personalised insurance plans

- Real-time health monitoring

- Digital medical records integration

Insurance companies are increasingly focusing on preventive healthcare and wellness programs to improve customer health outcomes.

Conclusion

Exploring www.nivabupa.com

is a practical starting point for anyone looking to buy health insurance in India. The platform provides a wide range of policies designed for individuals, families, and senior citizens. From affordable entry-level plans to premium coverage options, Niva Bupa aims to provide flexible healthcare protection. Features like cashless hospitalization, digital consultations, wellness rewards, and comprehensive medical coverage make these policies attractive to many customers.

However, choosing the right health insurance requires careful comparison of coverage limits, premiums, hospital networks, and policy benefits. By reviewing these factors and exploring plan comparisons on the official website, individuals can select a policy that aligns with their health needs and financial goals. Ultimately, a good health insurance plan is not just a financial product—it is a safety net that protects you and your family during unexpected medical emergencies.